Are you frustrated with standard, one-size-fits-all financial plans that don’t quite fit your unique needs? Whether you’re managing your own finances or handling the budget for your family, navigating the complexities of budgeting, saving, and investing can often feel overwhelming.

At Life Tree Planner, we recognize the challenges of creating a budget that reflects both your immediate needs and long-term goals. With years of experience in financial planning and management, we are here to help you tailor a plan that works for you.

In this article, we will explore:

- How to craft a detailed annual budget

- Effective strategies for managing and reviewing monthly transactions

- Examples of common expenses and income sources

- Investment and retirement planning tips

- Best practices for managing financial documents and making major financial decisions

- Techniques for building financial resilience and achieving long-term stability

Ready to take control of your financial future? Continue reading to discover practical advice and actionable steps that will help you build a secure and prosperous financial life.

By following our expert guidance, you’ll be well on your way to achieving a well-organized financial plan that supports both your current lifestyle and future aspirations.

- What is a budget and how do you create one?

- 3 Common types of budgets

- 3. The envelope method

- Crafting an Annual Budget in Detail

- Writing and Reviewing All Transactions Monthly

- Examples of Common Expenses

- Examples of Common Income Sources

- Investment and Retirement Planning Tips

- Tips for Managing Financial Documents and Records

- Steps for Making Major Financial Decisions

- Strategies for Building Financial Resilience and Security

- Managing Debt: Effective Strategies

- Achieving Long-Term Financial Stability

- Benefits of Emergency Funds and Savings

- 3 Ways to Teach Children About Money Management

- Integrating Financial Planning in Daily Life

- Balancing Immediate Needs with Future Goals

- Money Management: A Recap

What is a budget and how do you create one?

A budget is a plan that outlines how to allocate your income to cover expenses, savings, and debt payments. To create a budget, start by listing all your sources of income and then decide on your necessary expenses such as rent, utilities, and groceries.

Track your spending to see where your money goes and identify areas where you can cut back. Set realistic goals for saving money and paying off debt. Use money management tips to help you stick to your budget, such as setting up separate accounts for savings and expenses.

Regularly review your budget to track your progress and adjust as needed, ensuring you stay on the path to financial stability and avoid unnecessary worry.

- Income:

- Money received from various sources, such as salary, wages, bonuses, freelance work, investments, and rental income.

- Expenses:

- Money spent on daily living costs, including housing, transportation, food, healthcare, and debt repayments.

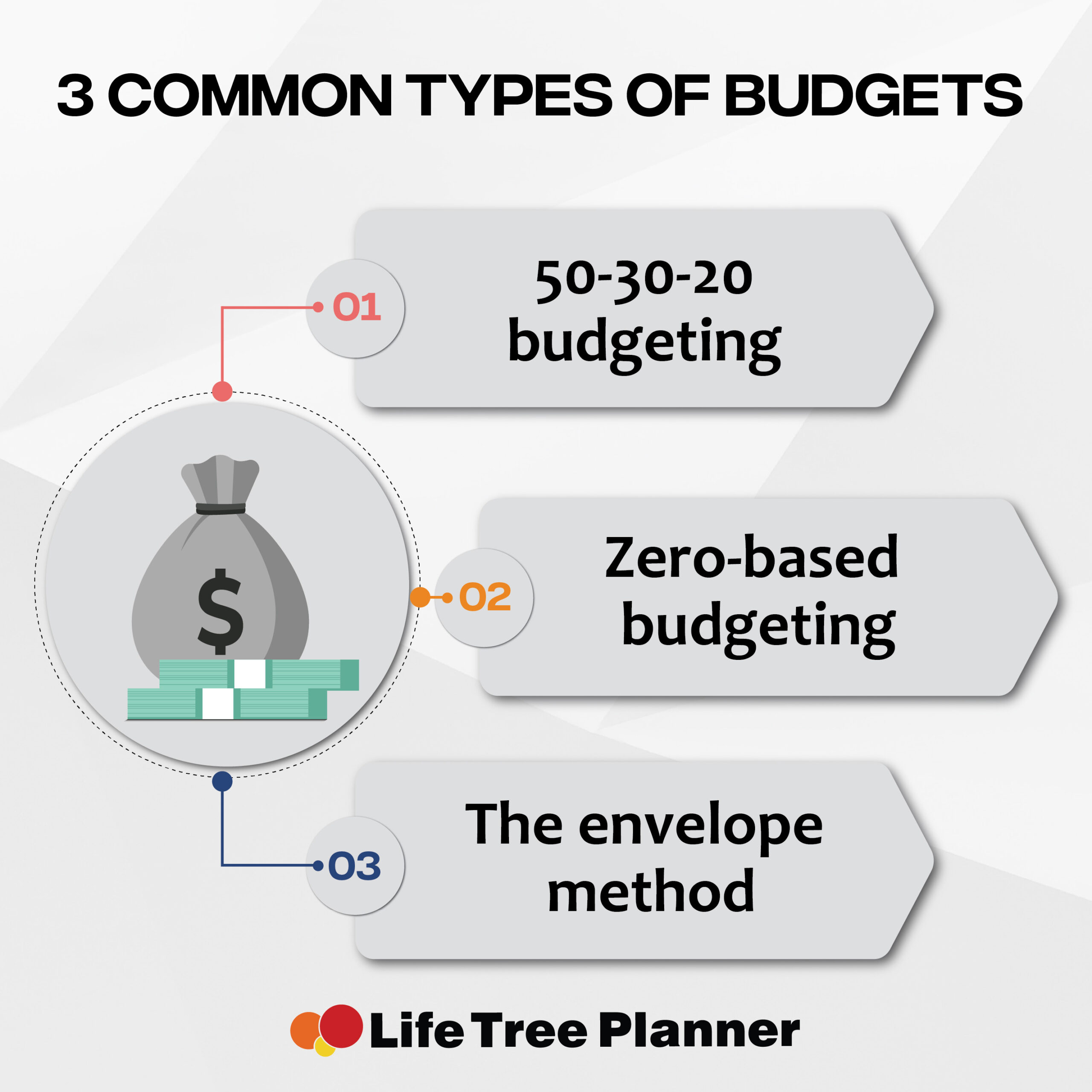

3 Common types of budgets

There are several methods for budgeting that you can use to help stay on top of your finances. But here are three popular ones:

1. 50-30-20 budgeting

The 50-30-20 budgeting rule is a simple yet effective personal finance strategy. It allocates 50% of your income to needs, such as housing, utilities, and minimum payments on debt. Next, 30% goes to wants, like dining out, entertainment, and hobbies.

Finally, 20% is dedicated to saving money and debt repayment. This method helps manage money by keeping spending habits in check and ensuring you pay necessary expenses while saving.

By using this rule, you can improve your money management skills, efficiently allocate funds in your bank account, and work towards debt consolidation and financial stability. It’s a versatile approach that supports both short-term spending and long-term financial goals.

2. Zero-based budgeting

Zero-based budgeting is a money management strategy ideal for young adults aiming to improve their personal finance skills. This method involves starting from scratch each month, with every dollar accounted for. Begin by creating a budget that covers all expenses and savings goals.

Allocate your income to categories like rent, groceries, and savings, ensuring your bank account reflects these decisions.

Tracking your spending habits helps you stick to the budget, adjust minimum payments, and avoid unnecessary expenses. Regularly review your progress and make adjustments as needed. This disciplined approach promotes saving money and better cash management, setting you on a stable financial path without the worry of overspending.

3. The envelope method

The envelope method is a practical money management tool, especially beneficial for young adults aiming to manage their money effectively and avoid debt.

This method involves dividing your monthly take-home pay into different categories of expenses, such as groceries, rent, and entertainment, and placing the allotted amount of money for each category into separate envelopes.

By spending only what’s in each envelope, you can avoid overspending and ensure you have enough money for all necessary expenses. This technique helps build good credit habits by preventing late fees and high-interest rates from unpaid debt.

It’s a straightforward way to manage your money, control spending, and potentially save extra money each month.

Crafting an Annual Budget in Detail

Creating an annual budget is essential for mapping out your financial journey. It allows you to estimate your income, wages, and expenses, helping ensure you stay on track to meet your financial goals.

Predicting and Tracking Annual Incomes, Wages, and Expenses

To begin, estimate your total income for the year and categorize your expenses.

Personal Example

- Total Income Estimate:

- Salary: $60,000

- Freelance Work: $5,000

- Investments: $2,000

- Total Income: $67,000

- Categorized Expenses:

- Groceries: $4,800

- Utilities:

- Electricity: $1,000

- Water: $500

- Internet: $600

- Health/Medical:

- Insurance: $2,400

- Medications and Doctor Visits: $800

Family Example

- Total Income Estimate:

- Combined Salaries: $90,000

- Rental Income: $6,000

- Total Income: $96,000

- Categorized Expenses:

- Groceries: $7,200

- Utilities:

- Electricity: $1,200

- Water: $600

- Internet: $800

- Health/Medical:

- Insurance: $3,000

- Medications and Doctor Visits: $1,200

Predicting Net Savings and Ending Balance Every Month

Calculate your monthly net savings and ending balances to ensure alignment with your financial goals. Regularly reviewing these figures helps you stay on track throughout the year.

Writing and Reviewing All Transactions Monthly

Maintaining a detailed record of transactions is crucial for effective financial management.

Compare Planned and Actual Expenses

Compare your planned budget with actual spending to identify discrepancies.

Personal Example:

- Planned Groceries: $400

- Actual Groceries: $450

- Discrepancy: $50

Family Example:

- Planned Childcare: $1,000

- Actual Childcare: $1,100

- Discrepancy: $100

Adjust and Update the Annual Budget Quarterly

Review and adjust your budget every quarter to reflect any changes in income or expenses.

Examples of Common Expenses

Understanding common expenses helps in creating a realistic budget. Here are some typical categories:

For Families:

- Children:

- Education: $2,000

- Childcare: $6,000

- Activities: $1,200

- Car:

- Maintenance: $800

- Insurance: $1,500

- Fuel: $1,200

- Entertainment:

- Family Vacations: $3,000

- Dining Out: $2,000

- Groceries: $7,200

- Utilities:

- Electricity: $1,200

- Water: $600

- Internet: $800

- Health/Medical:

- Insurance: $3,000

- Medications and Doctor Visits: $1,200

- Pets:

- Food: $800

- Veterinary Care: $600

- Debt:

- Mortgage: $12,000

- Personal Loans: $2,400

For Single Persons:

- Children: None

- Car:

- Maintenance: $500

- Insurance: $1,200

- Fuel: $1,000

- Entertainment:

- Movies and Dining Out: $1,500

- Groceries: $4,800

- Utilities:

- Electricity: $1,000

- Water: $500

- Internet: $600

- Health/Medical:

- Insurance: $2,400

- Medications and Doctor Visits: $800

- Pets:

- Food: $600

- Veterinary Care: $500

- Debt:

- Credit Card Payments: $1,200

- Student Loan: $2,000

See also Financial Management Techniques: 8 Strategies for Success

Examples of Common Income Sources

Identifying your income sources is crucial for budgeting. Here are some common sources:

For Families:

- Rent: Income from rental properties: $6,000

- Salaries: Combined family salaries: $90,000

- Contracts: Freelance or contract work: $6,000

For Single Persons:

- Rent: Income from rental properties: $6,000

- Salaries: Regular employment wages: $60,000

- Contracts: Freelance work: $5,000

Investment and Retirement Planning Tips

Investment and retirement planning are vital for long-term financial security. Here’s how to approach them:

Planning Tips

- Budget for Retirement:

- Personal Example: Allocate 15% of your monthly salary to retirement savings.

- Family Example: Allocate $500 monthly to a family retirement account.

- Explore Investment Options:

- Personal Example: Invest in a mix of stocks and mutual funds.

- Family Example: Diversify investments with real estate and index funds.

- Maintain Good Credit:

- Personal Example: Regularly check your credit report and pay off credit card balances on time.

- Family Example: Ensure all family members manage their credit scores responsibly.

Tips for Managing Financial Documents and Records

Efficient handling of financial documents is crucial for effective money management.

Document Management Tips

- Organize Records:

- Personal Example: Use a digital storage system for tax documents and receipts.

- Family Example: Keep separate folders for each family member’s financial documents.

- Review Regularly:

- Personal Example: Schedule a bi-annual review of your financial documents.

- Family Example: Review and update family financial documents quarterly.

- Maintain an Emergency Fund:

- Personal Example: Save at least three months’ worth of living expenses.

- Family Example: Build an emergency fund with six months of household expenses.

Steps for Making Major Financial Decisions

Major financial decisions, such as buying a house or pursuing higher education, can have significant financial implications.

Decision-Making Tips

- Evaluate Credit:

- Personal Example: Check your credit score before applying for a new car loan.

- Family Example: Review family credit scores before applying for a mortgage.

- Plan for Extra Costs:

- Personal Example: Budget for moving expenses when relocating for a new job.

- Family Example: Set aside funds for home repairs and property taxes.

- Make Informed Choices:

- Personal Example: Research investment options before purchasing stocks.

- Family Example: Consider long-term impacts of buying a larger home on family finances.

Strategies for Building Financial Resilience and Security

Building financial resilience involves strategies like budgeting, saving, and investing. It ensures stability and helps weather economic uncertainties.

Resilience Strategies

- Set Savings Goals:

- Personal Example: Save for a new car or vacation.

- Family Example: Save for family vacations or children’s education.

- Generate Extra Income:

- Personal Example: Take on freelance work or a part-time job.

- Family Example: Explore side businesses or rental income opportunities.

- Manage Risks:

- Personal Example: Purchase health and disability insurance.

- Family Example: Ensure adequate family health, life, and property insurance coverage.

Managing Debt: Effective Strategies

Effective debt management involves strategic planning and disciplined financial habits.

Debt Management Tips

- Build an Emergency Fund:

- Personal Example: Save to cover three months of expenses.

- Family Example: Save for at least six months of family expenses.

- Prioritize High-Interest Debt:

- Personal Example: Focus on paying off credit card debt first.

- Family Example: Pay down high-interest credit cards and personal loans.

- Consider Consolidation:

- Personal Example: Explore consolidating student loans into a lower-interest option.

- Family Example: Look into consolidating multiple family loans into a single lower-interest loan.

Achieving Long-Term Financial Stability

Achieving long-term financial stability requires strategic planning and disciplined execution.

Stability Tips

- Track Finances:

- Personal Example: Use a budgeting app to monitor monthly expenses.

- Family Example: Regularly review family expenses and income with budgeting tools.

- Automate Savings:

- Personal Example: Set up automatic transfers to a savings account.

- Family Example: Automate savings for family goals like vacations or education.

- Leverage Opportunities:

- Personal Example: Utilize employer-matched retirement contributions.

- Family Example: Take advantage of tax-advantaged savings accounts for family needs.

Benefits of Emergency Funds and Savings

Maintaining emergency funds and savings is crucial for financial stability and provides a buffer during crises.

Savings Tips

- Regular Contributions:

- Personal Example: Consistently deposit a portion of each paycheck into savings.

- Family Example: Allocate a set amount from family income to emergency savings each month.

- Prioritize Savings:

- Personal Example: Focus on building an emergency fund before discretionary spending.

- Family Example

Prioritize saving for emergencies and family goals over non-essential expenses.

- Invest Wisely:

- Personal Example: Choose investments that grow your personal wealth over time.

- Family Example: Invest in long-term growth opportunities for family financial security.

3 Ways to Teach Children About Money Management

Teaching children about money management sets a strong foundation for their future financial independence.

Teaching Tips

- Encourage Saving:

- Personal Example: Open a savings account and set savings goals.

- Family Example: Help children open savings accounts and teach them to set financial goals.

- Educate on Spending:

- Personal Example: Create a simple budget for personal expenses and savings.

- Family Example: Involve children in family budgeting activities to teach responsible spending.

- Discuss Credit:

- Personal Example: Explain the basics of credit and how to use it responsibly.

- Family Example: Teach children about credit cards and the importance of managing credit wisely.

Integrating Financial Planning in Daily Life

Incorporating financial planning into daily routines helps build healthy financial habits.

Planning Tips

- Pay Yourself First:

- Personal Example: Automatically transfer funds to savings before covering other expenses.

- Family Example: Ensure a portion of family income is saved or invested before spending.

- Set Specific Goals:

- Personal Example: Save for specific objectives like a vacation or a new gadget.

- Family Example: Set and track savings goals for family vacations or home improvements.

- Automate Savings:

- Personal Example: Set up automatic transfers to a savings or investment account.

- Family Example: Implement automatic savings for family goals and expenses.

Balancing Immediate Needs with Future Goals

Balancing current expenses with future aspirations requires careful budgeting and planning.

Balancing Tips

- Allocate Funds:

- Personal Example: Budget for current expenses while setting aside funds for future goals.

- Family Example: Allocate a portion of the family budget for immediate needs and long-term savings.

- Automate Savings:

- Personal Example: Use automatic transfers to manage both immediate expenses and future savings.

- Family Example: Set up automated savings for family goals alongside managing current expenses.

- Strategic Investments:

- Personal Example: Invest in assets that support both short-term needs and long-term objectives.

- Family Example: Choose investments that address both immediate family needs and future financial stability.

See also Money Management Books: 12 Must-Reads for Building Wealth

Money Management: A Recap

Effective money management for young adults is crucial to achieve financial stability. By understanding your monthly income and deciding on a clear path for your finances, you can reduce worry and stress.

Prioritize paying off debt and save regularly to build a secure future. Managing your money wisely involves tracking spending, ensuring you have enough money for necessities, and setting aside extra money for savings or investments.

Developing good credit habits and being mindful of interest rates will help you maintain financial health. With discipline and planning, you can manage your monthly take-home pay effectively, paving the way for a secure financial future.